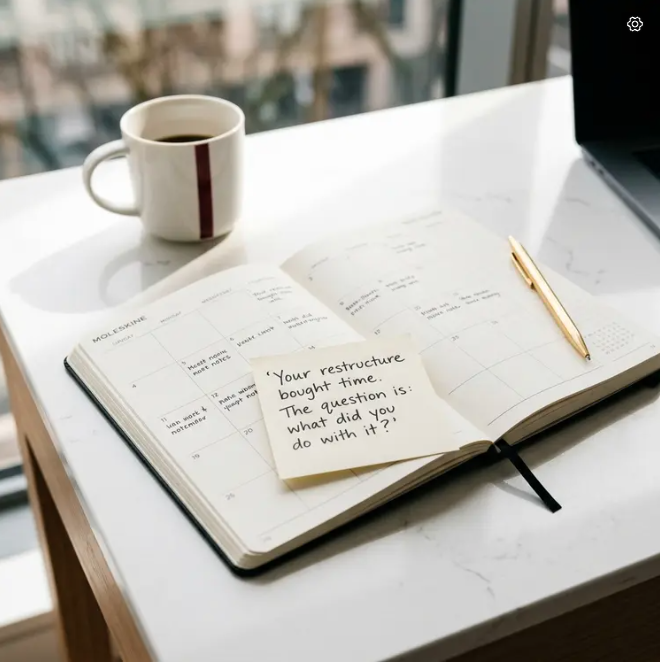

When you see headlines saying “Canadian homeowners are managing rising rates,” you’re getting half the story. The part they’re not telling you is what “managing” costs and how long it lasts.

I’m seeing more clients in Stoney Creek, Ontario struggling to keep up with monthly payments. Higher interest rates, increased cost of living, and economic pressure have many borrowers stretched. But here’s what the data doesn’t capture: the difference between managing payments today and having a structure that works 12 to 18 months from now.

That gap is where the real story lives.

The Mathematics Nobody’s Talking About

Start with what happens when someone’s mortgage payment doubles. You’re not looking at income versus mortgage. You’re mapping out the full picture. Mortgage, unsecured debt, car payments, taxes, credit cards, lines of credit, basic living costs.

After everything is laid out, you’re usually dealing with one of three realities.

There’s still some structure to work with. They have equity, decent credit, and manageable debt. This is where you stretch amortization if possible, consolidate high-interest debt into the mortgage, or refinance to lower total monthly obligations. But even here, you’re not saving money. You’re buying breathing room.

It’s tight, but not broken. This is the most common outcome. Income hasn’t kept up, debts are higher, and rates did the damage. After everything is laid out, there’s very little excess cash flow. You’re moving balances around to reduce monthly strain, prioritizing which debts must be paid down versus carried, possibly using short-term solutions if available. You’re not fixing the problem completely. You’re managing the pressure.

There’s no room left. After reviewing everything, there’s no way to lower payments enough. The conversation shifts to selling or downsizing, bringing in additional income or a co-borrower, or looking at insolvency options like a consumer proposal.

The hard truth is there isn’t a lot left to “optimize” once you break everything down.

How Long Does “Buying Time” Actually Last?

The “bought time” window is shorter than most clients, and honestly, most brokers, want to believe. From what shows up in practice, it tends to fall into a few rough timelines.

Short runway: 3 to 6 months. This is the client who was already on the edge before the payment shock. You consolidate, extend amortization, free up a few hundred a month, but nothing fundamentally changed. They start leaning on credit again. Small emergencies hit. Within a few months, they’re right back in the same position, sometimes worse.

Medium runway: 6 to 18 months. This is the most common outcome. You’ve created real breathing room. Payments are more manageable, debts are simplified, stress drops for a while. But if income hasn’t increased or spending hasn’t structurally changed, the math slowly catches up again. Balances creep back up, variable expenses rise, renewal or rate changes hit again. This is where they come back saying, “It was working until it wasn’t.”

Long runway: 2+ years. This only happens when something changes. Income increases, major debt gets paid down and stays down, or they adjust lifestyle meaningfully. At this point, you’re not buying time. You’ve shifted the trajectory.

The uncomfortable truth is if nothing meaningful changes beyond the restructure, most “pressure management” solutions have a lifespan of under 18 months.

Here’s the bigger issue: the second time they come back, you have fewer options, not more.

What the Data Shows Us

The numbers tell a story most people aren’t reading correctly. Holders of five-year fixed-rate mortgages renewing in 2025 or 2026 face an average payment increase of around 15% to 20% compared to December 2024 payments, according to Bank of Canada analysis. For borrowers renewing in 2025 with an average current rate of 3.60%, monthly payment increases are averaging $513.

But the aggregate view conceals pain. The remaining 40% of borrowers with mortgage rates rolling over from the ultra-low-rate period of late 2020 to early 2021 face payment increases, with the peak in renewals expected in Q4 2025 to Q1 2026.

Meanwhile, total consumer debt reached $2.62 trillion in Q3 2025, up 3.4% year-over-year, while average non-mortgage debt per consumer rose to $22,321, an increase of $511 year-over-year, according to Equifax Canada data. This suggests households are relying on credit to bridge monthly shortfalls.

The pattern I’m seeing in practice matches what the data is showing: when we free up credit through a consolidation, the debt is coming back a lot faster than people expect.

The 60-to-90-Day Reality

Right now, when we free up credit through a consolidation, you start seeing balances creep back within 60 to 90 days. By the six-month mark, a good portion of the available credit is already used again.

It’s not because clients are overspending. It’s because they’re still short every month.

Higher groceries, higher utilities, higher insurance, and overall cost of living haven’t come down. So even if we lower their mortgage payment, the rest of their life is still more expensive. What ends up happening is simple: they start using credit to cover the gap.

The consolidation creates relief on paper, but in reality, it just shifts where the pressure shows up. Instead of high payments, it becomes rising balances again.

Unless something changes, income goes up or expenses are reduced, the debt almost always comes back.

When the File Tells You It’s Over

A file is past the point of another restructure when the numbers stop improving no matter what you do with them.

You see debt was already consolidated once, now creeping back up again, sometimes close to where it started. The first solution didn’t change behavior or cash flow, it cleared space temporarily.

You see credit utilization climbing again within months. Not a year, not gradual. Fast. They’re still running a monthly shortfall and using credit as the buffer.

You see no real change in income, and no real reduction in expenses. Same job, same cost of living pressure, same household structure. Nothing in the equation has shifted.

You start noticing even if you push another refinance or consolidation, the payment relief is marginal. It doesn’t create breathing room. It rearranges the stress.

At this point, you’re not looking at a tough approval. You’re looking at a file where the system has already been reset once and immediately drifted back to the same place.

I stop asking “do we get this done” and start asking “why are we doing this again.”

The Markers That Tell You It Won’t Hold

There are a few markers I watch for right away telling me a restructure won’t hold, even if it gets approved.

If the payment only drops slightly, red flag. If we’re only saving them a couple hundred a month, it’s not enough to change behavior or stabilize anything.

If all we’re doing is rolling debt back into the mortgage and freeing up credit again, but there’s no plan or ability to keep those balances down, another one. The debt usually comes right back.

If their ratios are still tight after the restructure, meaning there’s no real buffer for life, car repairs, rate changes, anything unexpected, it’s not going to hold.

If income hasn’t changed and expenses haven’t been addressed, then nothing fundamentally improved. Same pressure, different arrangement.

And a big one: if we’re using up the last of their equity to make the deal work. Usually the final lever. Once gone, nowhere left to go.

When I see those together, I already know this isn’t a solution. Time is running out.

The Conversation Nobody Wants to Have

For me, it comes down to one question: does this fix anything, or am I buying them a few more months?

If I restructure it and there’s a real impact, lower payments, stabilized cash flow, and a path forward, then I’ll push it through.

But if the numbers show nothing’s changing, and they’re likely going to be back in the same position in 6 to 12 months, I don’t move forward because it gets approved.

You have to be honest.

At this point, you’re not helping. You’re delaying a bigger problem. And usually making it worse by adding more cost, more debt, and using up whatever equity they had left.

The decision isn’t about approval. It’s about outcome.

If the outcome doesn’t improve their situation in a real way, then it’s time to stop restructuring and look at a different move.

What Actually Shifts People

The biggest resistance is hope. Not denial. Hope there’s still one more restructure, one more lender, one more adjustment to make it work without having to make a bigger change.

Most clients are willing to tolerate stress as long as they believe it’s temporary. So they’ll often lean into “one more thing,” even when the numbers already showed them the last solution didn’t hold.

What shifts them isn’t pressure. It’s clarity.

It usually happens when a few things line up at the same time. They realize the last restructure didn’t solve anything, it delayed the problem. They see, in black and white, even if you reduce payments again, the gap still exists every month. They start to understand there’s no remaining lever to meaningfully change the outcome.

The moment it lands is usually quiet. It’s not emotional. It’s recognition.

The conversation stops being “do we fix this again” and becomes “what’s the most controlled way out of this position.”

Selling stops feeling like giving up at this point. It starts to look like containing damage, protecting equity, stopping the cycle, resetting before the situation erodes further.

Usually the real turning point: when they stop asking for another solution and start asking what prevents it from getting worse.

The Question You Should Be Asking Right Now

“If nothing about my income or expenses changes, will this structure still work in 12 to 18 months, or am I buying time?”

That’s the real filter.

Because what I’m seeing right now is people asking “do we make this payment lower?” instead of “does this solve the gap between what I earn and what my life costs?”

If the answer depends on credit being available again, or equity being used again, or rates improving again, then it’s not a solution. It’s a delay.

The files ending up back at the table six months later all have the same thing in common: the first restructure only worked if nothing went wrong after it.

The better question is whether the structure still holds if nothing goes right either.

If the honest answer is no, then the decision isn’t about whether you get approved today. It’s about whether you’re setting yourself up to revisit the same problem under worse conditions later.

Are you managing the pressure, or are you delaying the conversation you’ll need to have eventually?